Understanding the Two Models Through a Financial Lens

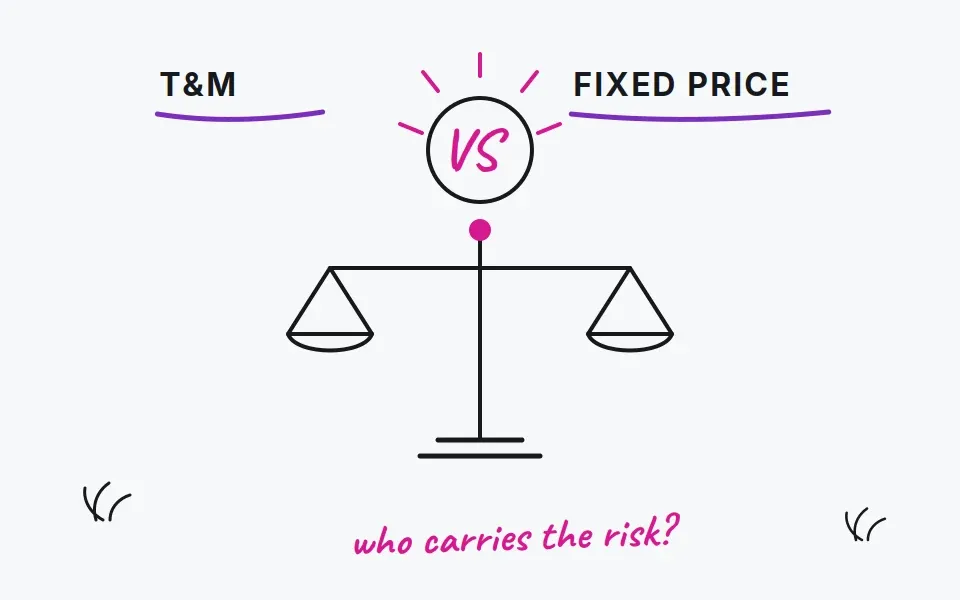

Fixed Price Contracts: Apparent Certainty, Hidden Variables

A fixed price contract sets a single, predetermined total cost for the entire project before work begins. The appeal is obvious: the client pays a known amount, the service provider delivers a defined scope, and the budget line stays clean on paper.

However, the fixed price model only works as advertised when the project scope is completely stable and requirements are fully defined upfront. In custom software development, that is rarely the case. Requirements evolve. Technologies shift. Business priorities change mid-build. When those things happen inside a fixed price agreement, the financial exposure does not disappear - it just moves.

Here is the mechanism most finance teams miss: vendors building fixed price projects routinely embed a 15 to 30 percent risk premium into their quoted price to protect themselves against uncertainty. This is an industry-standard buffer that clients pay regardless of whether those risks materialize. So even before a single line of code is written, a fixed price contract may already cost significantly more than an equivalent time and materials engagement.

There are also structural limitations to consider. Fixed price contracts require a long and detailed planning phase before work begins. Every requirement must be documented, agreed upon, and locked in. Change order management becomes administratively complex and expensive. When the project evolves - and in software, it almost always does - clients face a difficult choice: pay for expensive change requests, or accept a final product that no longer reflects their actual needs.

Fixed price contracts offer genuine benefits in the right context. They provide upfront budget visibility. They transfer cost overrun risk to the vendor. They simplify internal approval processes because the total cost is known at signing. For well-defined projects with a stable scope and fixed deadlines, they can be the right choice.

However, the key phrase is well-defined scope. Without it, the apparent certainty of a fixed fee contract quickly becomes an illusion.

Fixed Price Contract: Pros and Cons at a Glance

| Pros | Cons |

Upfront budget certainty and a known final price | Risk premium of 15 to 30 percent is typically embedded in the final price |

Vendor absorbs cost overrun risk within the agreed scope | Inflexible when project requirements change after signing |

Simpler internal approval and CapEx planning | Change requests are costly and generate contract disputes |

Less ongoing client involvement required during development | Requires exhaustive upfront documentation before work can start |

Higher risk of project failure if collaboration is discouraged to protect margins |